Keynote Remarks Delivered by Dr. Jean Rogers, SASB Founder

April 27, 2017,Kent State University

It is an honour to be here at the Annual Meonske Professional Development Conference. I’m Jean Rogers, and in 2011, I founded an organisation called the Sustainability Accounting Standards Board, or SASB. Today I will attempt to explain how sustainability accounting is relevant to your role as management accountants.

I know what you’re thinking: there’s financial accounting, tax accounting, forensic accounting, and of course management accounting, but sustainability accounting? Really? I’m here to tell you … it’s a thing. It is a lens through which corporate management can understand how critical dimensions of sustainability affect corporate performance. How global sustainability challenges, such as climate risk, resource constraints, changes in workforce composition, and stakeholder concerns, can affect a company’s ability to sustain and create value over the long term. And how dependent a company is on the forms of capital that it is competing for—beyond financial capital, which is often not a constraint to growth. Bain estimates that global financial capital has more than tripled over the past three decades and now stands at roughly 10 times global GDP. But access to high quality environmental capital and social capital can often be the overriding factor in securing a company’s future. Think Uber and workforce relations, or United Airlines and customer welfare. Sustainability accounting has evolved over the past several decades to describe a company’s performance on material environmental, social, and governance factors for the benefit of investors and society.

My aim today is to demonstrate that sustainability issues are in fact material to business, of interest to investors, and germane to management accountants.

Sustainability accounting shares several things with management accounting. First, it’s performance-based. The parameters being measured are often non-financial, not to say they are not related to financial performance, but they are measured in non-monetary units such as energy intensity in manufacturing, water consumption in beverages or agriculture, or safety data in transportation industries. Second, it’s quantitative and can be benchmarked. That means companies can establish a baseline, set targets, and track year-on-year improvements. That also means it can be subject to controls and assurance to produce reliable data from which to base decisions. Notice that I mentioned the industry where each parameter is particularly relevant. That’s another thing management accounting and sustainability accounting share: the measurements that yield the most decision-useful information are often industry specific.

Both a management accountant and a sustainability accountant measure a company’s risk exposure and its progress in implementing its strategy, and need tailored metrics to do so in a way that’s appropriate for each industry. SASB develops industry-specific standards that give rise to material sustainability data. Because topics like climate risk, product safety, and even human capital management, look different at an operational level from industry to industry—just like inventory, or the forecast of unit sales, or the impact of strikes are measured and reported in different ways.

Both management accounting and sustainability accounting provide a more holistic view of performance than financials can provide. In today’s knowledge-driven economy, a company’s ability to succeed relies increasingly on intangible assets—things like patents, processes, brand value, intellectual capital, and customer or supplier relationships. Among the S&P 500, for example, intangibles now account for more than 80% of market capitalization.

The measurements are directly related to value creation. You may be surprised to learn that sustainability accounting measurements are directly related to financial parameters and can be mapped to specific elements of a DCF. For example, for oil and gas companies, impact to current valuations can be approximated by discounting future expenses associated with carbon taxes or credit fees associated with direct emissions, as well as potential reductions in revenues, resulting from reduced demand and the associated commodity price impacts (such as those forecast by the IEA in its World Energy Outlook). Sustainability accounting data can be interrogated and interpreted (just like financial data) and used to better understand the relative health and competitive positioning of the organisation. Like management accounting data, these are often leading indicators of financial performance.

The rigorous practice of sustainability accounting de novo allows a complete reappraisal of the relative significance of social, environmental, and economic risks and benefits to corporate performance. You might say that sustainability accounting is a subset of management accounting.

So, instead of asking (which I know some of you did when I came up on stage) why would we want to measure this, the real question is, why wouldn’t we want to measure this? Why wouldn’t we want to know where we stand on material sustainability related matters in order to mitigate risks and drive better performance? Why wouldn’t we want to know which form of capital (environmental, social, or financial) is the limiting factor to our growth or which form of capital has a higher cost to the organisation?

The IMA has long been a leader in empowering management accountants to drive an organisation’s strategy and value amid unpredictable circumstances. The IMA has also been an early supporter of the need to account for all types of capital. As a 2008 IMA report called “The Evolution of Accountability: Sustainability Reporting for Accountants” explained: “The management accountant who fails to identify the factors contributing to the sustainability of the organisation is not providing management with a full picture of the organisation’s value or of the breadth of risks that need to be addressed in maintaining and enhancing the organisation’s value.”

Fundamentally, the IMA is founded on the premise that what gets measured gets managed. That’s exactly what we are doing at SASB. Creating a new literacy, for investors and corporate management alike, to manage topics that drive value, identify risks, and assess future prospects. Sustainability accounting can provide insight on where resources are being wasted and how a company can further improve its operational efficiency. It can help management accountants develop insight into cost drivers and create more robust activity-based costing analyses. And because SASB metrics are tied to specific value impacts, they fit neatly into a balanced scorecard approach to performance evaluation.

Now that I have hopefully convinced you that sustainability accounting is not just for Earth Day but for every day, I’d like to provide some specifics about SASB and how our standards are designed and enable the measurement and management of material topics related to business.

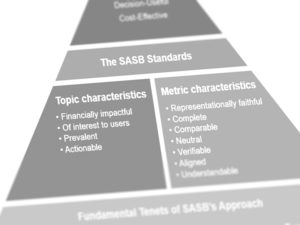

SASB is an independent 501c3 nonprofit based in San Francisco. Our mission is to develop and disseminate sustainability accounting standards that help public corporations disclose material, decision-useful information to investors in a way that is cost-effective. We accomplish this mission through a rigorous process that includes evidence-based research, broad, balanced stakeholder participation, public transparency, and independent oversight. We specifically develop our standards so that they are aligned with US securities laws and can be used in mandatory SEC filings. On average, there are just five topics per industry included in the standards.

We believe that all investors have a right to comparable disclosure on material sustainability factors without the need to source it from CSR reports and questionnaires or purchase it from commercial vendors. We also believe all investors should be able to type in a ticker and compare sustainability fundamentals to financial fundamentals – this is the world that SASB enables.

The vision for SASB was developed at the Initiative for Responsible Investment at Harvard University, based on research going back a decade and first published in a paper called “From Transparency to Performance.” In the early 2000s there was an explosion of sustainability reporting, the glossy reports that are ubiquitous today and prepared by many of your companies, but not always tied to business goals. Awards cropped up for “best report” but not best performance. Can you imagine a parallel in financial reporting?

Interestingly, there was a time when the accounting profession faced a similar crisis. In 1972, the Wheat Commission studied the relationship of accountants to their clients, and found a strong positive bias in opinions. Against a backdrop of significant M&A activity, accountants had become cheerleaders for their clients and opinion shopping was prevalent. This, among other factors, precipitated the creation of the FASB in 1973. Lacking accounting standards, the field of sustainability reporting faces a similar bias. Read any corporate sustainability report—it’s designed to share stories with a broad range of stakeholders, including customers, employees, NGOs, journalists, and vendors. It’s PR. It is not designed to provide a true and fair representation of performance for investors. In fact, a 2013 study by Olivier Boiral in the Accounting, Auditing, & Accountability Journal found that over 90% of known negative events are not reported by companies in their sustainability reports. It’s not uncommon for a company to spend several hundred thousand dollars on a sustainability report every year. According to Verdantix data, there is a $877M annual market in sustainability reporting services, and that doesn’t capture what companies themselves are spending. All this time and money is being spent on voluntary CSR reports, but investors still do not have the information they need to make investment decisions.

If these reports were doing the trick for investors, we wouldn’t be here today. I often hear from controllers and internal auditors that investors don’t seem to care about this information. Well, all I have to say is that you need to get out more. Investors are making their demands known from the boardroom, to investor relations, to the sustainability department, to the SEC. They are urgently asking for a market standard because the unreliable, unaudited, uncontrolled, incomparable and biassed information they get in sustainability reports isn’t sufficient for investment decisions. Let me give you a few examples of investor demand, and the ways they are expressing investor interest.

Increasingly, mainstream investors are interested in this information. For them, the lens is materiality. If sustainability factors affect the financial condition or operating performance of companies, they therefore affect investor decisions on whether to buy, sell, or hold a security. In a 2015 CFA Institute survey, 73% of institutional investors indicated that they take environmental, social and governance issues into account in their investment analysis and decisions to help manage investment risks. 89% of the world’s top 100 asset managers are signatories to the Principles for Responsible Investment (PRI). This is not boutique investing. And what they need is data.

One example of investors expressing demand for improved sustainability disclosure is SASB’s new Investor Advisory Group (IAG). The IAG comprises 28 leading asset owners and asset managers with more than $20T in assets, including BlackRock, CalPERS, CalSTRS, and State Street Global Advisors. The IAG is educating companies about investor use of environmental, social, and governance information and asking companies to use SASB standards to guide ESG disclosure.

There’s a disconnect between investor demand for improved ESG disclosure and the corporate response to this demand: while 100% of corporates are confident in the quality of ESG information they report, only 29% of investors are confident in the quality of the ESG information they receive. Because of the lack of decision-useful information in existing sustainability disclosures, investors resort to other means of getting data and assessing performance. The number of sustainability-related shareholder proposals filed each year continues to rise. In 2016, 67% of resolutions filed related to ESG issues.

This situation isn’t working for companies either. Companies face disclosure fatigue from requests coming from investors, NGOs, and ratings agencies. For example, in 2014, GE reports that it developed responses to more than 650 requests from ratings groups alone. GE says the process took several months and involved more than 75 people across the organisation with little benefit to GE and its shareholders. On a 2016 IMA webinar, close to 100 companies reported filling out more than 250 ESG surveys per year. This scenario is not uncommon, and is a tremendous waste of corporate resources, not to mention liability—if any of it is material, there is such a thing called Regulation F-D.

SASB is here to provide a solution. We take an industry-specific approach to sustainability accounting—provisional standards are available for 79 industries. This is essential because sustainability issues manifest themselves differently from one industry to the next. Take climate change as an example. Just seven out of 79 industries (the number of industries in SASB’s industry classification system, which is called SICS) account for 85% of the Scope 1 carbon emissions from public equities. The remaining 72 industries are certainly impacted by climate risk, but not because of the threat of a societal or regulatory response to their carbon emissions. For apparel companies, what is important is the ability to source cotton, a crop that is vulnerable to shifting weather patterns. For commercial banks, it is their financed emissions: loans to oil and gas companies, industrials, utilities, and other industries whose own risk exposures could threaten their ability to repay or refinance. For automakers, it is progress on developing alternative-fuel vehicles to respond to shifting consumer demand patterns.

SASB helps investors integrate sustainability considerations into their investment strategies at the company, sector, and portfolio levels. Ultimately, the standards enable investors to more efficiently allocate capital. For example, by breaking down climate change into its specific impacts, SASB helps investors understand which industries will be facing headwinds because of global sustainability challenges so they can diversify their portfolios through sector allocation. Meanwhile, comparable data allows investors to perform more robust benchmarking and valuation, helping to identify leaders and laggards on specific sustainability issues and to determine which companies are well positioned to address these material factors.

Securities law is very clear in its articulation of materiality as relevant to the reasonable investor, and that is what drives our analysis of material factors at SASB for the purposes of standards setting. If performance on a sustainability topic does not have a demonstrated link to value, it is not in our standards. These are the issues that are likely to be considered by mainstream analysts and investors. If they don’t see evidence of impact that would move the needle on a DCF over a 5-year time horizon, it’s not included. And that’s important because immaterial information does not belong in a 10-K.

And that leads us to the current state of disclosure on these topics. I’m often challenged by folks like you; if material information is required to be disclosed by Regulation S-K, are you saying that companies are breaking the law? Well, not exactly.

Recent research by SASB shows that 69% of companies are already addressing at least three-quarters of SASB disclosure topics for their industry, and 38% are already providing disclosure on all SASB disclosure topics. When companies address these issues in their Form 10-K or 20-F, it is a clear indication that they consider the risk to be material and the information to be relevant to investors. However, more than half of sustainability-related disclosures in SEC filings use boilerplate language, which is inadequate for investment decision-making.

Let’s look more deeply into the substance of our standards, with a few industry examples. These are material issues that often have poor disclosure and are likely not being well managed.

Counterfeit Drugs is a topic that is in our standards in both Pharma and Biotech. The World Health Organization estimates that the global market for counterfeit drugs has reached $431 billion, representing one percent of the US’s supply, and 10-15% of the world’s pharmaceuticals market. An International Policy Network report suggests that fake tuberculosis and malaria drugs alone cause 700,000 deaths annually. This is not only an issue in emerging markets. In 2012, fake Avastin was distributed to pharmacies and doctors in the US. Avastin, a cancer medication produced by Roche Holdings’ Genentech division, typically sells for $2,400 per 400-milligram vial. According to the Pharmaceutical Security Institute, cancer drugs currently rank eighth among the top ten types of drugs being counterfeited (the top is genitourinary followed by anti-infectives and central nervous system). Counterfeiters are beginning to target more expensive drugs (but any drug can be a target), presenting a significant threat to industry revenues in addition to consumer welfare.

Of the top ten Pharma and Biotech companies, only one provides metrics in their annual SEC filings. Let me give you an example of a typical disclosure (Pfizer 2015 10-K): “We undertake significant efforts to counteract the threats associated with counterfeit medicines…. No assurance can be given, however, that our efforts and the efforts of others will be entirely successful, and the presence of counterfeit medicines may continue to increase.” In contrast, here’s an example of a disclosure using metrics (GSK 2015 20-Y): “Patient and consumer safety… We strive to minimise the risk of counterfeit medicines. In 2015, we extended our end-to-end supply chain serialisation programme, Fingerprint, across 86 packaging lines in more than 18 manufacturing sites. The programme applies unique serial ‘fingerprints’ on products and logs them into a government-managed database, which they can be verified against at any point in the supply chain.”

Food Safety is a topic that’s in our standards in Restaurants. Recently, Chipotle’s stock lost 32% of its value ($7B) over 2½ months when the restaurant chain was struck by outbreaks of E. coli and norovirus that left more than 500 sickened across 12 states. But it’s not just an issue for Chipotle—looking at 60 companies throughout the food supply chain over the past 25 years, one report found that restaurant share prices are significantly impacted by food safety incidents. For Jack in the Box in 1993, Yum Brands in 2006, and Chipotle in 2015, same store sales declined in the quarter in which they faced an E. coli outbreak and remained depressed for several quarters after.

Regarding disclosure of the top companies by revenue, 40% use boilerplate to describe their food safety records. Consider this example of boilerplate disclosure, from the 2015 10-K pf BJ’s Restaurants: “Although we have followed industry standard food safety protocols in the past and continue to enhance our food safety and quality assurance procedures, no food safety protocols can completely eliminate the risk of food-borne illness in any restaurant. Even if food-borne illnesses arise from conditions outside of our control, the negative publicity from any such illnesses is likely to be significant. If our restaurant customers or employees become ill from food-borne illnesses, we could be forced to temporarily close the affected restaurants.”

Safety metrics are interesting. They can’t tell you when a serious event will happen, but they certainly can tell you if there is a pattern of volatility and whether it is on management’s radar. Analysts would adjust for a risk that is present but not being managed by a premium on the cost of capital.

Product Safety in Automobiles is also in our standards. There has been a lot of news lately about airbags, but did you know how significant this is across the industry? Can anyone guess what percentage of cars sold on an annual basis are recalled in the US? That’s a trick question – it’s not a percentage, it’s a multiple. For recalls between 2010 and 2014, six out of the nine major auto makers, at their highest point, recalled more than 3 times the number of cars sold in the US in the same year. One company recalled 9 times the number sold. What we have, in effect, is a US auto repair industry. But do you know what our auto industry analyst had to do to obtain this data? She had to get it from the National Highway Traffic Safety Administration, where it is routinely reported. But it is not a place that investors routinely go for information on material factors, when selecting an automotive stock.

Auto recalls affect both auto companies and auto parts manufacturers. Vehicles made by 19 different automakers have been recalled to replace airbags, made by Takata, in what is being called as the largest auto recall in history. Some of those airbags deployed explosively, injuring or even killing car occupants. Takata faces risk of bankruptcy for the air bag recalls. In January 2017, Takata pleaded guilty in the US; the criminal penalty alone is $1 billion.

The state of disclosure is 30% boilerplate on automotive safety issues. Here’s an example of boilerplate, from the 2015 10-K of Ford Motor Company: “Meeting or exceeding many government-mandated safety standards is costly and often technologically challenging, especially where standards may be in tension with the need to reduce vehicle weight in order to meet government-mandated emissions and fuel-economy standards.… Should we or government safety regulators determine that a safety or other defect or a noncompliance exists with respect to certain of our vehicles prior to the start of production, the launch of such vehicle could be delayed until such defect is remedied. The costs associated with any protracted delay in new model launches necessary to remedy such defects, or the cost of recall campaigns or warranty costs to remedy such defects in vehicles that have been sold, could be substantial.”

Lastly, let’s look at drug pricing in Pharma & Biotech. In 2016, concerns over pricing practices contributed to an 87% decrease in Valeant’s stock price, representing a loss of $85 billion in market value from its 2015 peak. Further, Mylan was forced to pay $465 million to settle allegations that it overcharged Medicaid for its EpiPen. The issue became a bipartisan rallying cry. In response, Allergan and Novo Nordisk announced that they would no longer raise individual drug prices by more than 10% within a year. While, Merck and J&J released reports on their pricing practices to enhance transparency.

How could our standards have helped to predict this material impact on stock price? By disclosing the rate of net drug price increases. Had investors had this data readily available, they would have seen that Valeant raised its prices 4 times the industry average in one year. Not 4% more but 4 TIMES the industry average price increase over its product portfolio, with one product being hiked 550%. Mylan was right up there too.

There’s a fine line between profitability and losing your license to operate when it comes to health care. Investors could have seen this one coming. Drug affordability is a material issue in health care, one that affects consumers, companies, and their investors. However, it is an issue with poor disclosure: in Biotech, 67% is no disclosure and 33% is boilerplate; and in Pharma, 30% is no disclosure and 40% is boilerplate.

SASB standards are a market solution to a market problem. In March 2016, SASB completed issuing provisional standards for 79 industries. Currently, SASB is in a period of deep consultation to gather additional input regarding the materiality of topics and usefulness of the metrics prior to codifying the standards in late 2017. Our process to codify and maintain the standards can be found in the SASB Rules of Procedure, a recently released governance document.

In conclusion, what’s next? Fortunately, everyone in this room can help move the markets. Management accountants have long helped lead their organisations in the ongoing quest to understand and measure what creates value, whether those factors are explicitly financial or not. SASB standards support both the evolution of business as it adapts to a changing world and the key role management accountants play in that evolution.

We must provide investors with the information they need to make informed decisions in today’s world. Sustainability accounting standards are the means to accomplish this goal. Through standards, we can modernise disclosure while protecting investors and facilitating efficient functioning of the markets and formation of capital. Through standards, we can ensure companies measure and manage the most critical sustainability issues of our time, creating a race to the top to improve performance. Managerial accountants’ focus on performance management and corporate strategy parallels sustainability accounting’s objective to draw the link between today’s performance and tomorrow’s ability to create value. The expertise and interest in this room represents a great opportunity to move this conversation forward. With standards, we can measure what needs to be managed, so that the markets can work efficiently and reward sustainable outcomes.